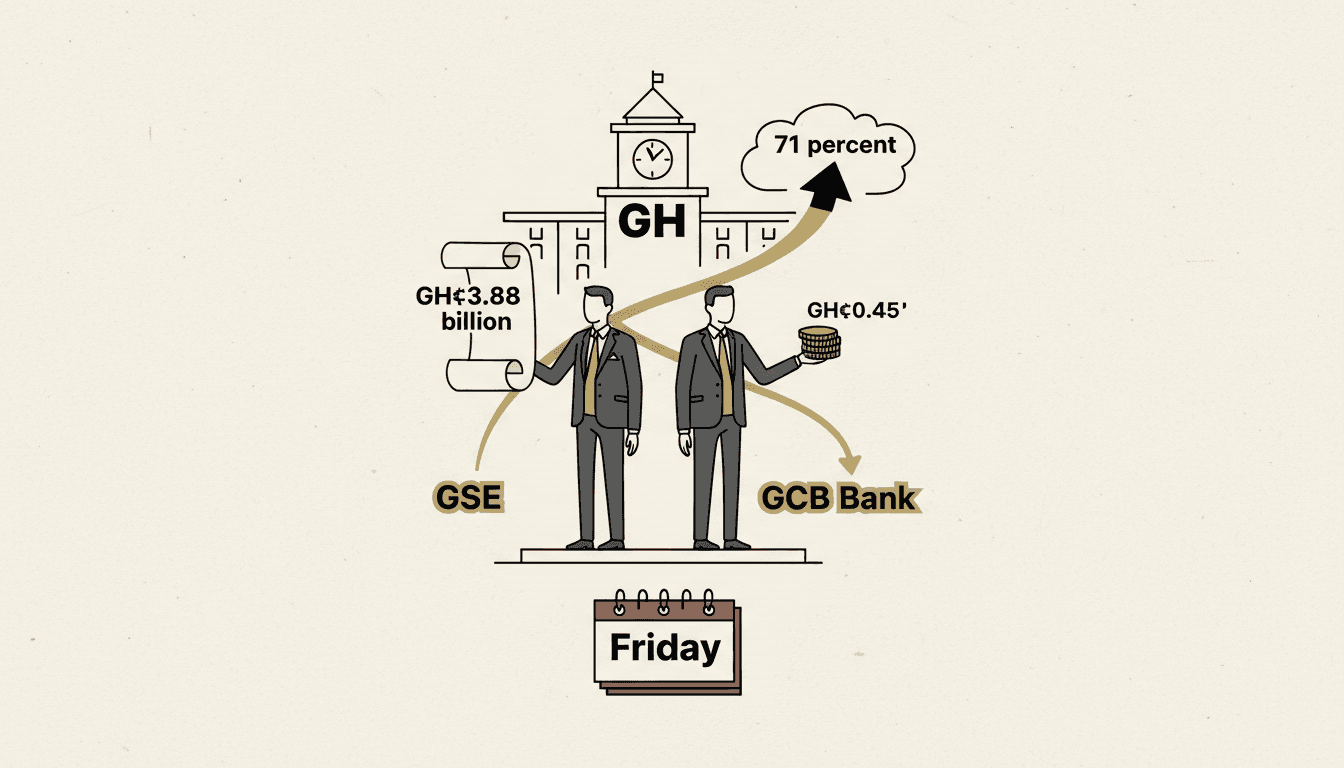

13,149.10. That is where the GSE Composite Index closed for the week on Thursday 10 April, up 42.58 points in the final session. The market gained on three of four trading days after the Easter break, adding approximately GH¢3.88 billion to total market capitalisation, which reached GH¢247.73 billion.

The Financial Stocks Index closed at 7,946.37, up 44.22 points. Year to date, the FSI is up 70.99 percent. The Composite Index is up 49.93 percent. Banking stocks are outperforming the broad market by 21 percentage points.

GCB Bank led Friday's gainers, rising GH¢0.45 to close at GH¢25.96. Over the full week, GCB gained approximately GH¢1.60. Ecobank Transnational added GH¢0.06 to GH¢1.67. MTN Ghana, which accounted for more than half of daily volume across most sessions, edged up GH¢0.01 to GH¢5.50. CalBank gained GH¢0.01 to GH¢0.75 on 700,215 shares traded.

TotalEnergies was the week's standout mover, surging GH¢2.56 on Monday's reopening and closing the week at GH¢38.09, up approximately GH¢3.45 from the pre-Easter level. Republic Bank was the largest Friday decliner, falling GH¢0.19 to GH¢4.51.

The YTD picture

The GSE has been Africa's best-performing securities market in 2026. In Q1, the Composite Index crossed 15,000 for the first time on 10 March, a 73 percent surge from the January open. It has since corrected but remains nearly 50 percent above where it started the year at approximately 8,770 points.

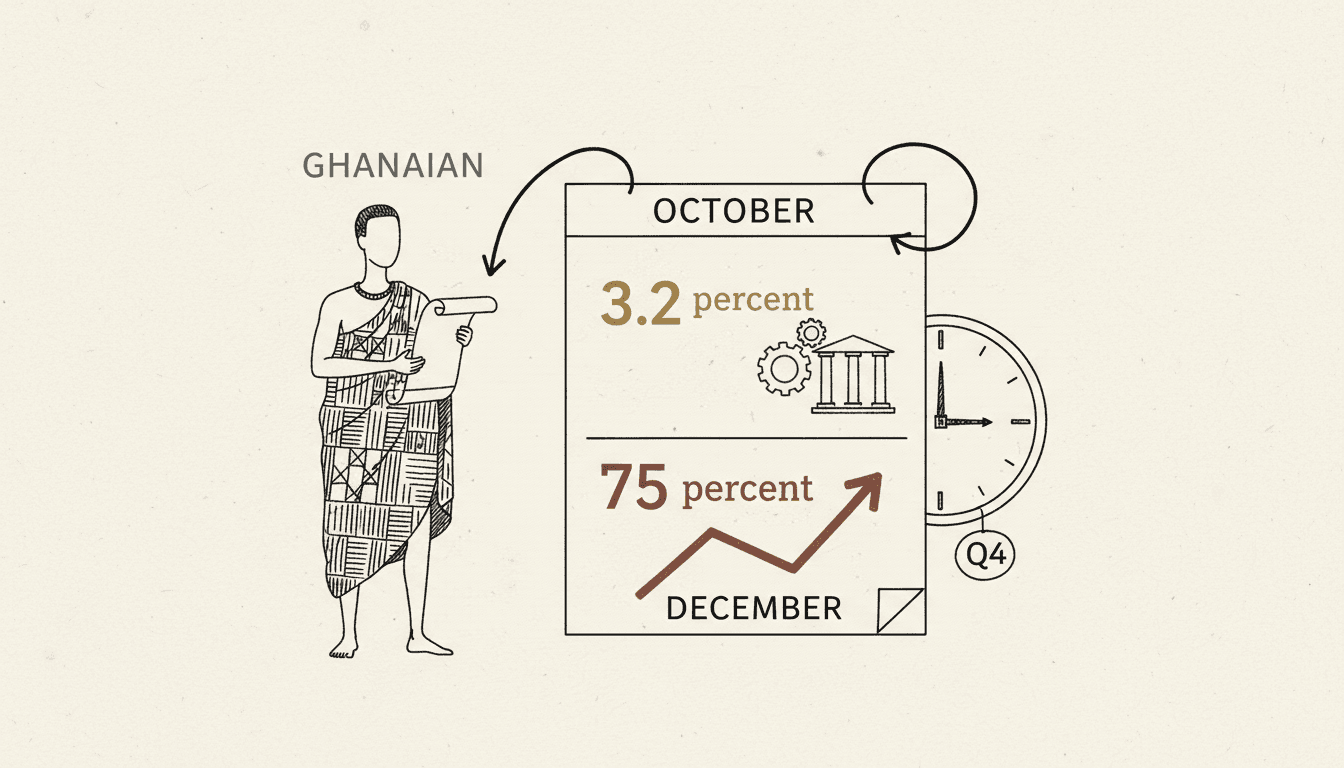

Trading value in early 2026 rose 113.9 percent year on year to GH¢38.26 billion. Databank expects the rally to extend through 2026, forecasting a 55 percent annual gain on the back of earnings momentum and the macro tailwinds: inflation at 3.2 percent, the policy rate at 14 percent, and institutional capital rotating from fixed income into equities as rates fall.

The First Atlantic Bank IPO in December 2025, which raised GH¢786 million and ended a seven-year listing drought, is cited by analysts as a confidence marker that could encourage further listings this year.

The Moody's timing

Moody's revised Ghana's outlook to positive on Friday 11 April, the day after the week's final trade. The market did not react to the announcement in real time. Whether the positive outlook — which signals a potential upgrade from Caa1 toward B3 over the next 12 to 18 months — translates into a Monday session rally will be visible on 14 April.

The GH¢2.7 billion 7-year bond issued in late March, Ghana's first since the DDEP moratorium expired, reopened the domestic yield curve. That is good for macro confidence and equity sentiment. It also means longer-dated bonds now compete with equities for institutional capital. For now, lingering DDEP caution is keeping much of that capital in Treasury bills rather than bonds, which means the equity inflow has not been drained. That balance is worth watching as the bond programme scales.