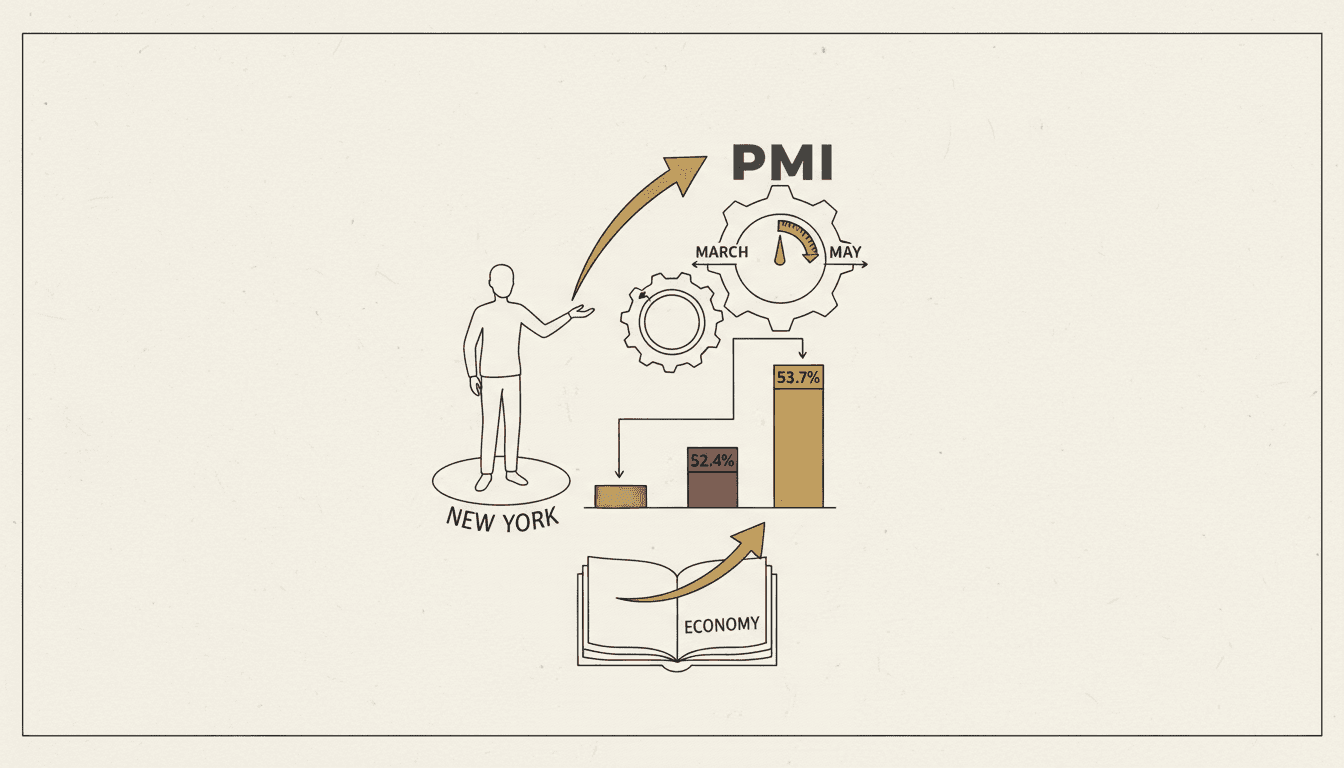

51.4. The S&P Global Ghana Purchasing Managers' Index returned to expansion in March 2026, rising from 49.2 in February and 48.5 in January. It is the first improvement in business conditions in three months and the most pronounced since May 2025.

New orders grew at their fastest pace since May 2025. Employment rose for the fourteenth consecutive month, at a faster rate than February. Purchasing activity returned to growth for the first time in three months. Output increased at a pace matching December 2025 as the joint-fastest in ten months.

The headline reads bullish. The sub-indices do not all agree.

The price signal

Private-sector firms have cut their selling prices for 11 consecutive months. March was the eleventh. The reduction was slightly shallower than February but the direction has not changed since May 2025.

Input costs fell again, supported by exchange rate stability, but the decline was marginal. Some firms reported higher fuel costs linked to the Gulf crisis. The gap between input costs falling slowly and selling prices falling persistently is a margin squeeze. Firms are pricing for volume, not profit. That works when demand is recovering. It becomes a problem if costs accelerate before margins rebuild.

S&P Global Economics Director Andrew Harker said the private sector has solid foundations to react to any disruption caused by the Middle East conflict, given the lack of inflationary pressures and a generally positive demand environment. But he noted initial concerns about the potential impact of the war on prices, with higher costs having the potential to throw growth off course.

Confidence is fading

Business confidence eased to an 11-month low in March despite the return to expansion. Firms remain optimistic that output will increase over the coming year, but the level of that optimism is the weakest it has been since April 2025. The Gulf crisis is the cited reason.

The split between current conditions (improving) and forward expectations (deteriorating) is the tension in this reading. The economy is expanding today but firms are less certain about tomorrow.

The African comparison

Nigeria's PMI led the continent at 53.2 in March, its sixteenth consecutive month of expansion. Ghana's 51.4 outperformed South Africa's 50.8. Kenya fell sharply to 47.7, its first contraction in seven months, dragged down by weak consumer spending and Middle East-driven cost pressures.

Ghana's position — expanding but cautious, disinflationary but not comfortable — is the middle ground. The 7.5 percent MIEG growth reading for January confirms the economy is growing in absolute terms. The PMI confirms the private sector is recovering in momentum terms. But 11 months of selling price cuts at 3.2 percent CPI inflation is closer to deflation than it is to the 8 percent target the Bank of Ghana considers neutral. That is a different kind of problem than the one Ghana had 15 months ago.