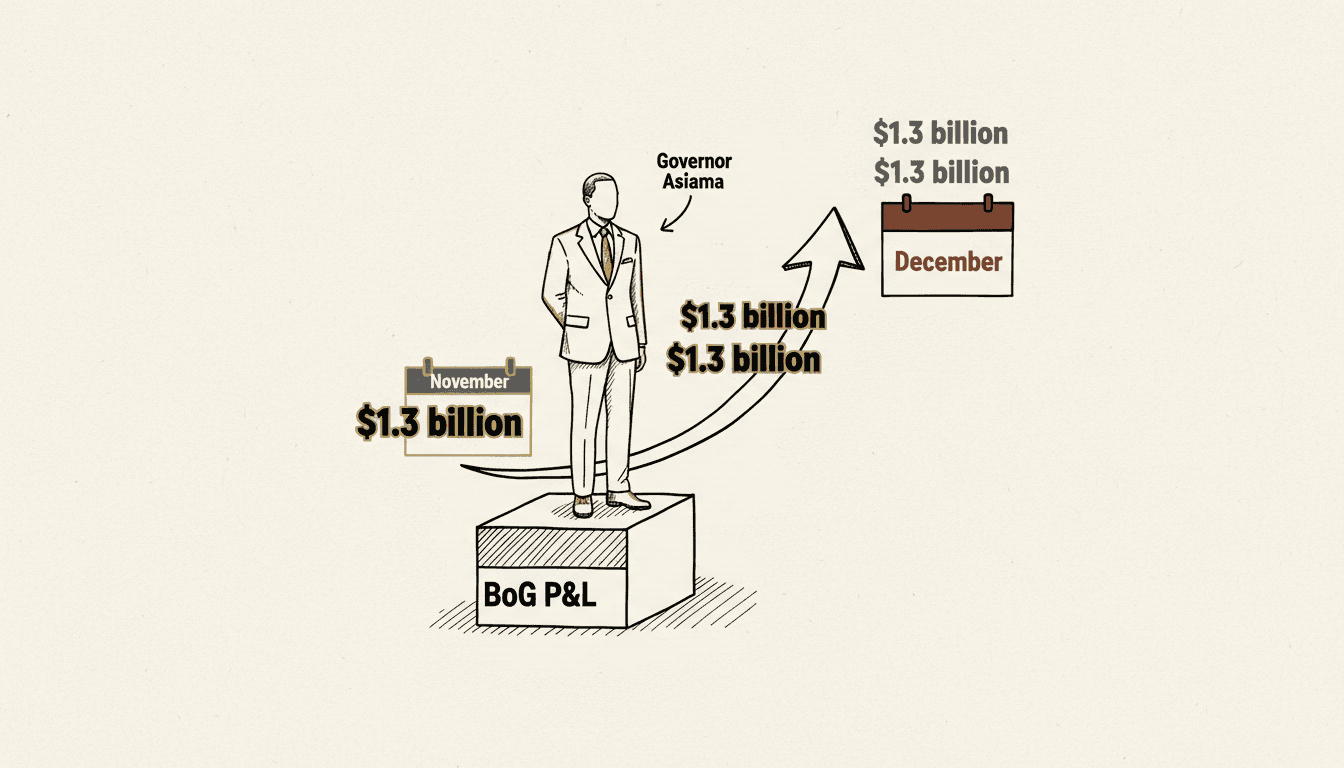

$1.3 billion. That is the realised profit the Bank of Ghana booked from selling roughly 19 tonnes of gold across November and December 2025, reducing its holdings from 37.1 tonnes to 18.1 tonnes, or about 51 percent of the pre-sale position. Governor Johnson Asiama confirmed the transaction at the 129th Monetary Policy Committee press briefing on 19 March. His framing was that the sale was portfolio rebalancing and the proceeds remained inside the country's international reserves.

The number underneath that number is whether the gain lands on the 2025 profit and loss statement. If it does, the 2025 result looks very different from the 2024 result.

Start with the loss history. The BoG booked a GH¢60 billion loss in 2022, when the sovereign debt restructuring forced a writedown on its government bond holdings. The 2024 number was a GH¢9.3 billion loss. The 2025 number, before audited statements close, was expected to be another significant loss. The central bank has been operating with negative equity since the 2022 sovereign default, and the recapitalisation arrangement worked out between the BoG, the Ministry of Finance, and the Ghana Cocoa and Gold Boards is structured to run through 2032. That pathway combines government bond issuance, the transfer of state-enterprise liabilities off the BoG balance sheet, and a sequence of measures that walk the central bank back to positive equity over a decade.

A $1.3 billion realised gain is materially larger than the 2024 loss. The recognition question is therefore the whole accounting story. If the gain is recognised in the 2025 statement, and if the Bank's auditors agree that a realised reserve transaction meets the recognition test rather than a valuation adjustment that would flow through other comprehensive income, then the 2025 P&L could be substantially closer to balance than the 2024 outcome. Realised gains on physical reserve sales typically do flow through the P&L. Valuation gains on unsold reserves typically do not. Asiama's framing — "the transaction made a profit of over $1.3 billion, and it is all within our international reserves" — leans toward the realised-gain interpretation.

That matters politically as well as accounting-wise. A central bank that produces a smaller loss in 2025 than in 2024 strengthens the government's argument that the IMF Extended Credit Facility programme is working. A near-balanced 2025 result strengthens it considerably more. The recapitalisation arithmetic through 2032 shifts in the same direction. None of those second-order outcomes happen automatically. The auditors will write the line that the political read depends on.

The strategic question Asiama's framing leaves open is why the BoG chose to crystallise the gain now rather than let the position run. Gold prices in late 2025 were inside a multi-month rally that did not look exhausted. Selling 51 percent of the position in two months, while gold was rising, traded a directional bet for a balance-sheet outcome. The Governor's portfolio-rebalancing language is the technically correct framing for that choice. The harder question is whether a central bank with the BoG's negative-equity position should have been running a directional bet on gold at all, given that the original accumulation was the consequence of an earlier balance-sheet management decision rather than a forecast on the metal.