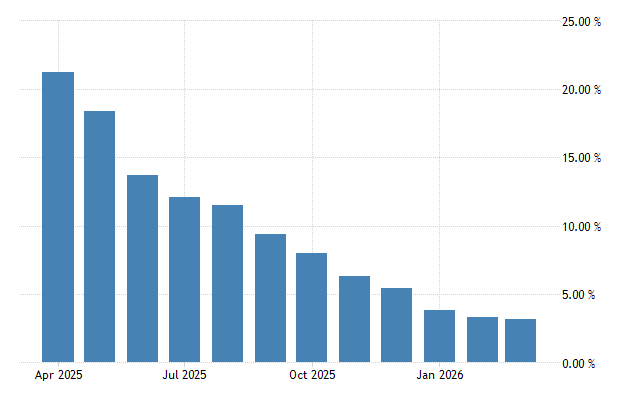

Headline inflation fell to 3.2% in March 2026. That is down from 22.4% in March 2025. It is the lowest reading since the Ghana Statistical Service rebased the consumer price index in 2021, and it marks the 15th consecutive month of declining inflation.

The number is worth sitting with. Twelve months ago, prices were rising at more than 22% annually. The economy was still absorbing the aftershocks of DDEP, and the cedi was under pressure. Today, inflation is within BoG's medium-term target band, and the central bank is cutting rates aggressively in response.

The exchange rate picture

The cedi is trading at an average of GHS 10.85 per dollar. Over the past month, the currency weakened 2.88% against the dollar. Over the past 12 months, it has appreciated 29.06%.

Both figures matter. The monthly depreciation suggests the cedi is no longer strengthening at the pace seen through most of 2025. The annual appreciation figure reflects how far the currency has recovered from the crisis levels of 2023-2024. Imported inflation, which drove much of the price surge during the crisis, has reversed course as the cedi regained ground.

The risk sits in the monthly trend. If the cedi continues to weaken at 2-3% per month, the annual appreciation figure will erode within two quarters, and imported price pressures will start feeding back into headline inflation. BoG's rate cuts make this more likely, not less. Lower domestic interest rates reduce the carry trade incentive for foreign capital, which weakens demand for the cedi.

Growth and banking stability

Real GDP grew 6.0% in 2025, a strong recovery number driven by mining output, services sector expansion, and improved agricultural performance. The IMF projects 4.8% for 2026, a moderation that reflects the fading of base effects and the normalisation of post-crisis rebound dynamics.

The banking sector's capital adequacy ratio stood at 17.5% as of December 2025, well above the 13% regulatory minimum. Banks rebuilt capital buffers through retained earnings during the high-interest-rate period, and asset quality has improved as the DDEP exchange offer settled. The sector is in its strongest position in three years.

What the 3.2% figure does and does not tell you

The disinflation is real but partly mechanical. The rebased CPI, updated weights, and base effects from the 2023-2024 price surge all contribute to the low headline number. Food inflation, which hits lower-income households hardest, has fallen but remains above the headline figure. Transport costs track fuel prices, which track the cedi and global crude. Neither is fully within domestic policy control.

The macro picture, taken whole, is the best it has been since before the debt crisis. Growth above 4%, inflation at 3.2%, a banking sector with adequate capital, and a central bank with room to ease. The question is durability. The last time the numbers looked this clean was 2021, and what followed was the worst economic crisis in a generation.

March 2026 inflation: 3.2%. The trend is clear. The test is whether it holds through the second half of the year.