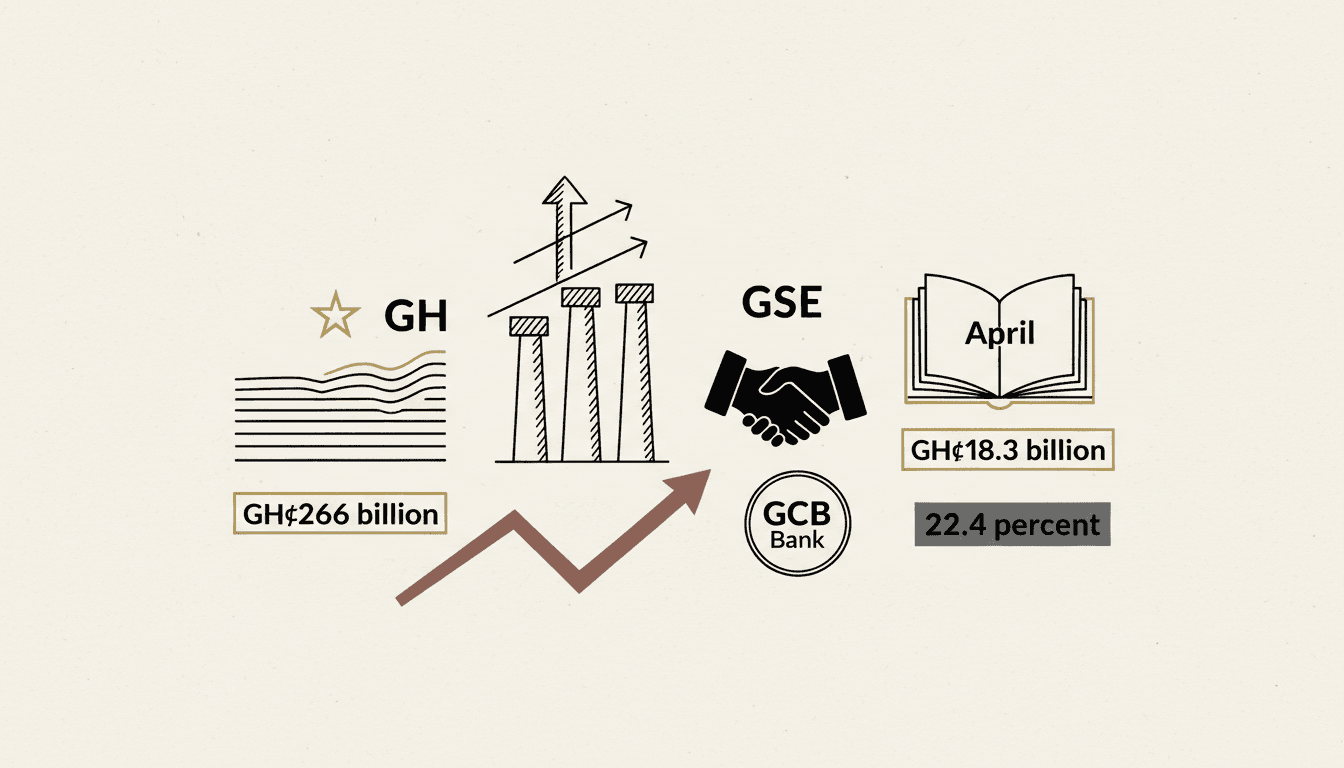

GH¢266 billion. That is where total market capitalisation closed for the week ending 17 April, up 7.5 percent from GH¢247.73 billion the previous week. The GSE Composite Index gained 357 points to close at 14,024.22. The Financial Stocks Index reached 8,314.05, up 242 points.

Trading volume surged 47 percent to 12.7 million shares worth approximately GH¢62.3 million. The ICT sector, led by MTN Ghana, accounted for over 64 percent of volume and 75 percent of total value traded.

The year-to-date numbers remain extraordinary. The Composite Index is up 55.8 percent. The Financial Stocks Index is up 73.7 percent. SIC Insurance has returned 272 percent. Republic Bank approximately 255 percent. Ghana Oil Company 162 percent. This is a market that has nearly doubled in four months.

Banking stocks are the story

GCB Bank surged GH¢5.81 to GH¢31.77, a 22.4 percent weekly gain. Ecobank Transnational added GH¢0.43 to GH¢2.10, up 25.8 percent. SIC Insurance gained GH¢0.90 to GH¢4.46, over 25 percent. CalBank rose 15 percent to GH¢0.86.

On the other side, Access Bank fell GH¢11.35 to GH¢30.65, a 27 percent decline. Benso Palm Plantation dropped 10 percent to GH¢89.99.

The banking rally has a structural explanation. The DDEP restructured GH¢31 billion in pension holdings and forced banks into recapitalisation. By end-2024, 13 banks that recorded capital deficits after the DDEP had largely restored their Capital Adequacy Ratios to 13 percent. Total banking assets expanded 33.8 percent in 2024. The sector has recovered from the debt exchange faster than most analysts expected, and the stock prices are repricing that recovery.

Where the money is rotating from

Pension funds, insurance companies, and institutional investors that were heavily concentrated in government securities before the DDEP are diversifying. The NPRA has intensified training for pension fund trustees on investment governance and portfolio diversification. The 5 percent alternative investment allocation now permitted under pension guidelines is creating a new capital pool for equities and private equity.

At the same time, T-bill yields have compressed to 4.91 percent on the 91-day while the policy rate sits at 14 percent. The gap between what government paper pays and what equities are returning is driving institutional money into the exchange. Databank forecasts a 55 percent annual gain for 2026 on the back of this rotation.