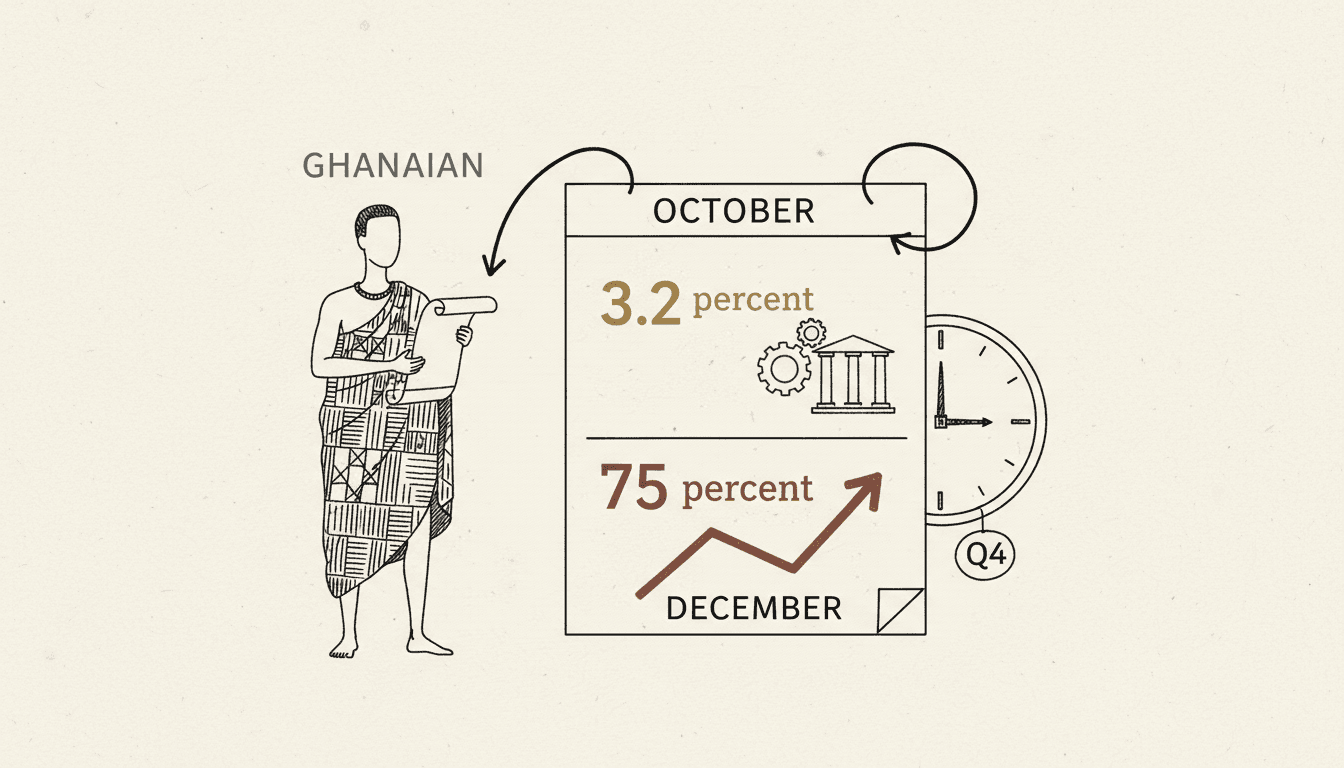

The Number: 3.2%

Headline inflation in March 2026. Down from 22.4% a year ago. This is the 15th consecutive month of disinflation and the lowest reading since the Ghana Statistical Service rebased the consumer price index in 2021.

The trajectory tells a clear story. In March 2025, prices were still rising at 22.4% year-on-year. Twelve months later, that figure has collapsed to 3.2%. The speed of the decline is as notable as the destination. Few forecasters projected single-digit inflation this early when the disinflation cycle began.

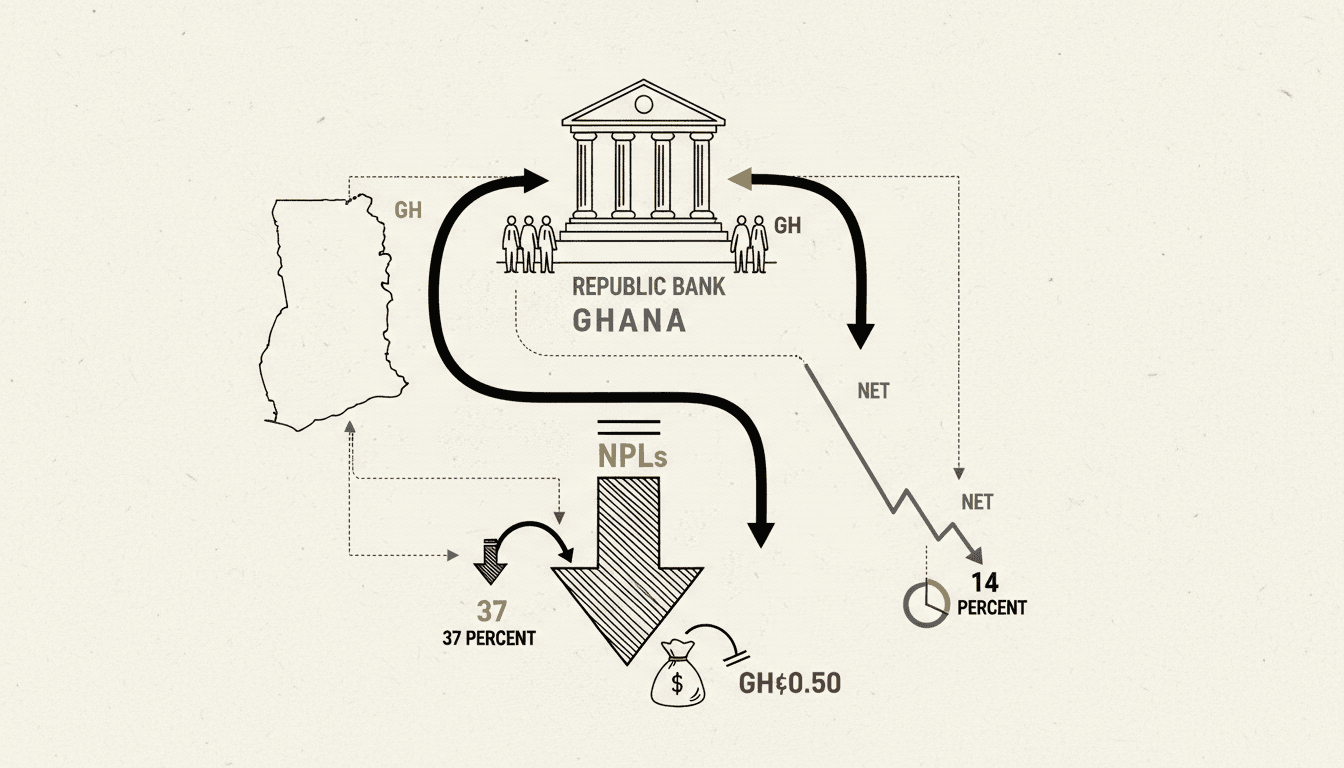

BoG's policy rate sits at 14%, which now represents a significant positive real rate. With inflation at 3.2%, the gap between the policy rate and headline inflation is the widest it has been in years. This creates room for rate cuts, and the market is pricing that expectation in. Bond yields have already begun adjusting downward.

For households, the relief is tangible but uneven. Food inflation, which disproportionately affects lower-income earners, has fallen but remains above the headline figure. Transport costs have stabilised following fuel price adjustments. Rent, the stickiest component of the basket, has been slower to respond.

For businesses, lower inflation reduces input cost uncertainty and makes planning easier. For banks, the positive real rate environment means deposit mobilisation becomes more attractive to savers, while the case for lending rate reductions strengthens.

The 15-month streak is the longest sustained disinflation run since before the 2022 crisis. The MPC meets next in May. The policy rate is 14%; inflation is 3.2%. That is an 1,080-basis-point gap, the widest in a decade.