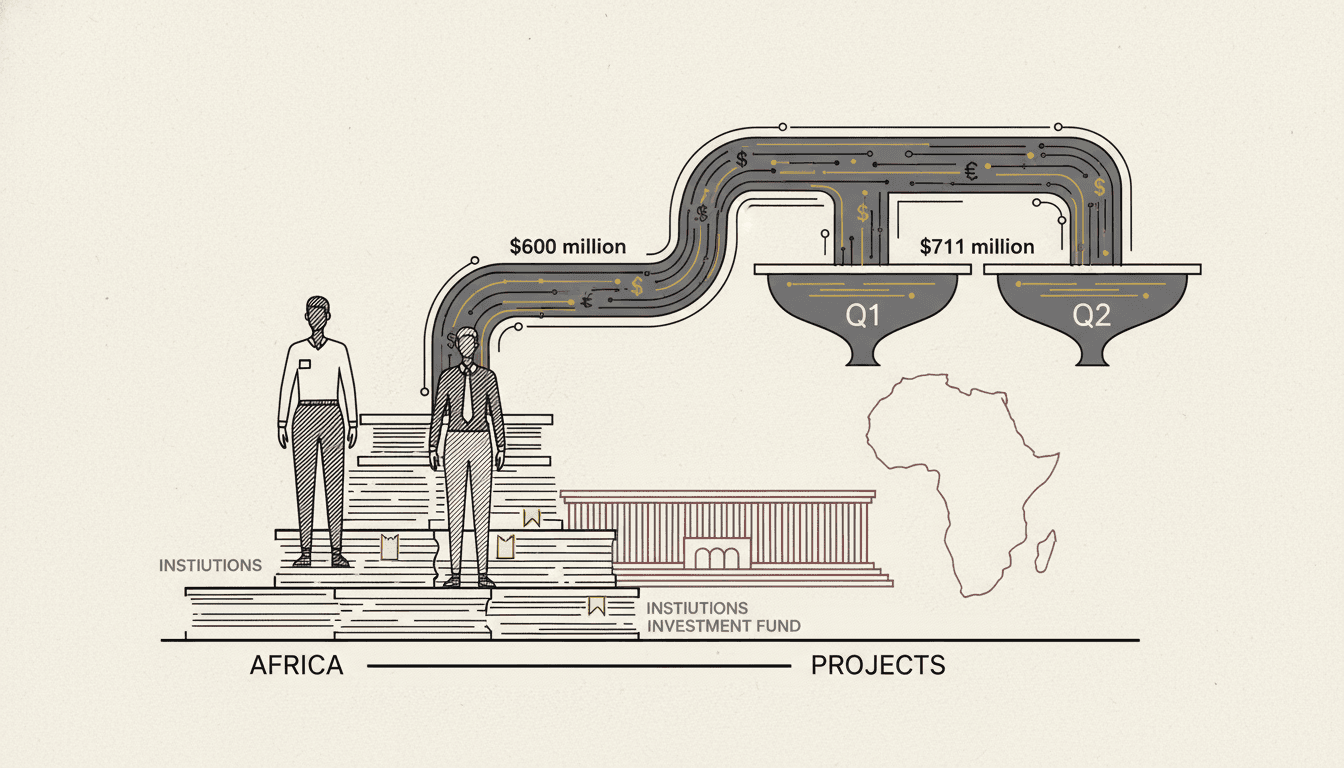

African startups raised between $600 million and $711 million in the first quarter of 2026, depending on whose tracker you read. Africa: The Big Deal counted $600 million across 83 ventures, with equity at $291 million and debt at $304 million. TechCabal Insights tracked $711 million across 80-plus deals, with 18 percent of deal values undisclosed. The methodologies are different. The directional conclusion is the same.

Both trackers put fintech at the top of the sector breakdown. TechCabal recorded $221 million into fintech for the quarter. Energy and water came in at $141 million; logistics and transport at $149 million. Sistema.bio's $53 million debt round, MNT-Halan's $40 million bond issuance, and Zeno's $25 million Series A were among the quarter's largest individual transactions per Big Deal. The geography was concentrated in Egypt at $154 million and South Africa at $134 million, with Kenya and Nigeria rounding out the top four. Ghana did not feature as a disclosed country in either tracker's top-tier breakdown.

The headline number is fine. The number underneath the headline is not. Big Deal's reading of March 2026 in particular was that only 22 startups raised $100,000 or more during the month. That is the lowest monthly deal count since the tracker began in 2021. The newsletter's own summary: "Only 130 ventures raised between $100k and $500k in equity in the past 12 months, and this is again the lowest that rolling count has been since at least 2021."

The distinction matters because dollar totals tell you what happened to a small number of companies that were already in a position to raise serious money. Deal count tells you what is happening to the rest of the funnel. Fewer small rounds being closed now is a leading indicator for fewer medium rounds in the next twelve months, because the companies that would have closed medium rounds are the ones that were supposed to have raised at $250,000 last year. The funding stack is front-loaded at the top and thinning at the bottom.

The composition is the second signal. Across Big Deal's Q1 figure, roughly half the capital was debt. MNT-Halan's contribution alone was a bond issuance. Debt-heavy quarters are normal in the middle of a tight equity market. Founders who cannot raise equity at acceptable dilution take on revenue-based or venture debt at higher cost. It is not a sign of distress at the individual company level. It is a sign of what the private capital market was charging for risk during the quarter. The continental read connects to a trend Ferviddy covered earlier in the year: fintech is no longer Africa's favourite bet, even as it remains the largest sector by quarterly dollar totals.

What the two trackers agree on is that M&A and expansion activity continued at a pace the early quarters of 2025 did not see. Thirty-plus M&A deals, eighteen-plus regional expansions. Flutterwave's acquisition of Mono was the headline M&A event. Moniepoint acquired Orda, which is the kind of scaling-through-acquisition move that establishes what the quarter's most capitalised operators are trying to build into. At the same time, the list of closures and restructurings — KOKO shutting down, Jumia exiting Algeria, Uber exiting Tanzania, Kuda layoffs, Zap Africa cutting 44 percent of its workforce — tells the other half of the same story.