MTN Nigeria suspended its Xtratime airtime and data credit advance service on 16 April. Airtel Nigeria followed on 17 April. Optasia, the JSE-listed fintech that provides airtime credit infrastructure, suspended services with at least one unnamed Nigerian operator the same week.

The suspensions were triggered by the Federal Competition and Consumer Protection Commission's Digital, Electronic, Online, or Non-Traditional Consumer Lending Regulations, passed in July 2025 with compliance deadlines that have been extended twice. On 2 April 2026, the FCCPC directed telecom operators to cease non-compliant lending services.

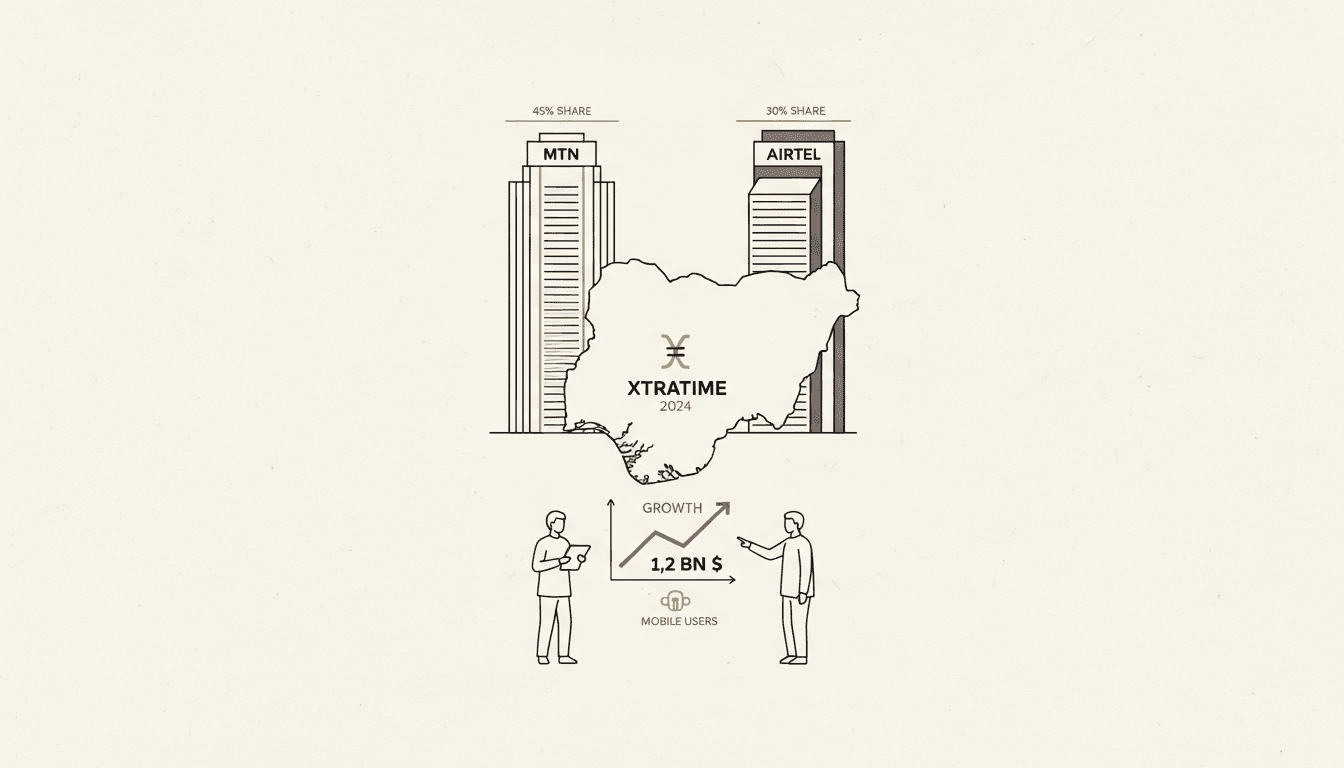

MTN's fintech revenue reached N191.3 billion ($142.5 million) in 2025, up 80 percent year on year. The company said the suspension is not expected to materially impact earnings.

What the regulations require

The DEON regulations mandate licensing for all digital lending services, full disclosure of interest rates, charges, and default fees, and handover of lending data to authorities within 48 hours of request. Fines reach up to N100 million or 1 percent of annual turnover. Directors involved in misconduct face five-year bans. By October 2025, 492 digital lenders had registered, up from fewer than 120 two years earlier.

The regulations were introduced after what the FCCPC described as a deluge of consumer complaints involving opaque charges, unexplained deductions, aggressive recovery practices, and poor disclosure standards.

The court challenge

The Wireless Application Service Providers Association of Nigeria secured an interim injunction at the Federal High Court in Lagos restraining the FCCPC from enforcing the regulations pending a hearing scheduled for 27 April. Justice A. Lewis-Allagoa barred the FCCPC from imposing sanctions, enforcing compliance directives, or issuing new instructions to WASPAN members.

Despite the injunction, airtime lending services remain suspended. The operators appear to be waiting for regulatory clarity before reactivating.

Who this hurts

Airtime lending is Nigeria's most widely used microloan product. Tens of millions of prepaid subscribers borrow airtime and data daily. Repayment is automatic — deducted from the next recharge. For low-income users, borrowed airtime is the difference between connectivity and silence. The suspension disproportionately affects the people furthest from formal banking.

The Ghana signal

Ghana's MTN MoMo Advance and Telecel airtime lending products are not affected. The FCCPC is a Nigerian regulator with no jurisdiction in Ghana. But the pattern across West Africa is converging: tighter fintech regulation, stricter agent compliance (BoG's AML/CFT agency guidelines), and more scrutiny of digital lending practices. If Ghana's Bank of Ghana or NCA moves in a similar direction, the airtime credit products that millions of Ghanaians use daily could face the same reckoning.