At least thirteen African fintechs have registered in Canada as Payment Service Providers or Money Services Businesses since early 2026. LemFi, Nala, Chimoney, Fincra, Payaza, ZuniQ, Rabafast, TaajPay, Aboki Finance, Bongo Payments, Raenest, Taptap Send, and Ghana's own WeWire are on the list. The pattern is a quiet but significant shift in where African fintechs domicile their North American operations.

WeWire — founded by Ebenezer Ghanney (CEO) and Desmond Nyamador (CTO) — has processed over $3 billion for 3,000 businesses across 80 countries. Its Canadian PSP licence lets it clear and settle as a regulated peer with Canadian financial institutions rather than as a third-party client.

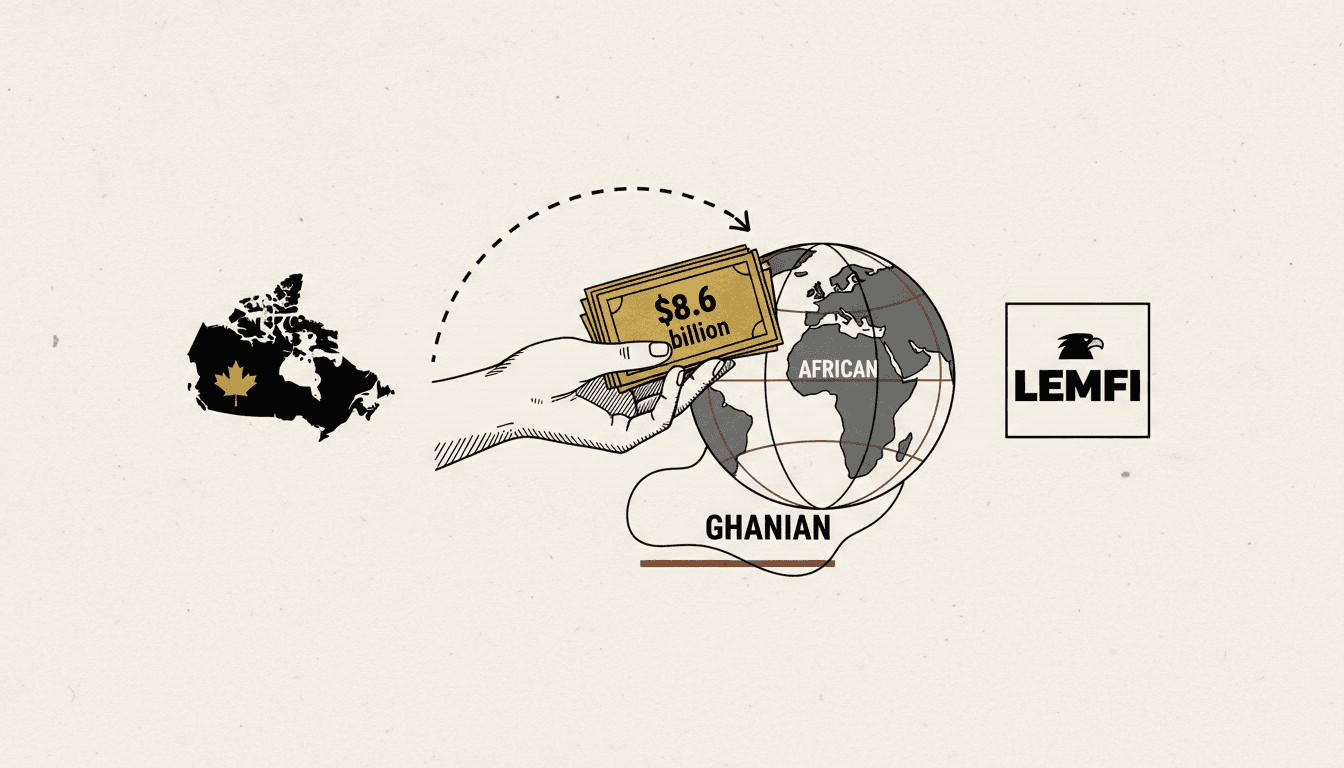

Why Canada

The federal structure is the first reason. One Bank of Canada PSP registration under the Retail Payment Activities Act covers Canada's 40 million people. The US requires state-by-state money transmitter licensing — up to 50 separate applications, each with its own capital requirements and fees. That alone is enough to redirect early-stage fintechs north.

The economics are the second reason. Canada's MSB registration through FINTRAC — the federal anti-money laundering agency — has no application fees and no minimum capital requirements. The PSP application costs approximately CAD $2,500. Penalties for non-compliance are serious: up to CAD $1 million for standard violations and CAD $10 million for fund-safeguarding failures. But entry is priced for startups.

The market is the third reason. Canada's diaspora remittance market runs at approximately CAD $8.6 billion annually, driven by Nigeria, Ghana, Ethiopia, Kenya, and francophone West African corridors. PSP status lets fintechs tap that flow as regulated counterparties rather than as customers paying spreads to incumbent banks.

Why not the US or UK

The US tightened fintech program oversight through 2025 as regulators pushed banks to scrutinise their fintech partnerships harder. State-by-state licensing costs scale linearly with geographic reach. The UK's FCA framework is credible but expensive, and post-Brexit clearing and correspondent banking access is more constrained than it was five years ago.

Canada has positioned itself as what LaunchBase described as a regulatory anchor jurisdiction amid EU MiCA implementation and enhanced US AML supervision. Two federal bills received Royal Assent on 26 March 2026 expanding Canada's AML/CFT framework. The first annual PSP reports were due 31 March 2026.

What this signals

The registration wave is not arbitrage. It is infrastructure. African fintechs — particularly remittance-focused players — need a regulated North American footprint to clear USD and CAD, maintain correspondent banking relationships, and avoid the de-risking wave that has closed correspondent accounts for African banks over the past decade.